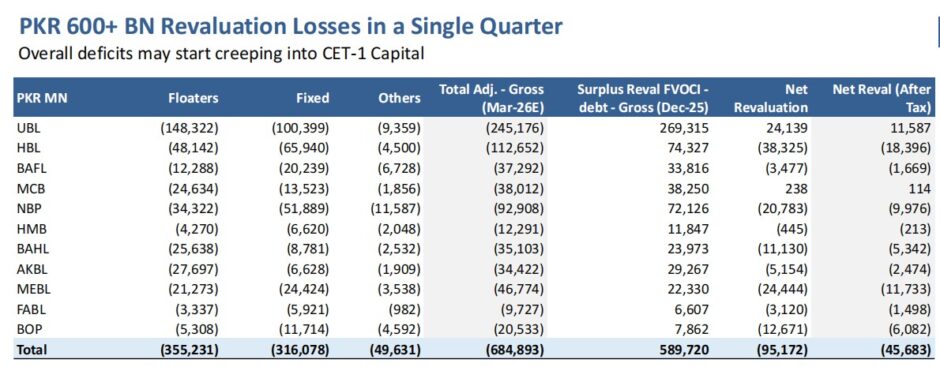

Pakistan’s banking sector is facing a sharp setback after posting more than Rs600 billion in revaluation losses in just one quarter. The decline comes as interest rates continue to rise, putting pressure on balance sheets and investor confidence, according to a research report released on April 6, 2026.

The report highlights growing risks across the sector. Higher bond yields are driving much of the stress. At the same time, banks are relying heavily on open market operations. This dependence has increased their exposure to short-term funding pressures. OMO borrowing now makes up around 24% of domestic debt, which raises concerns about system-wide stability.

Another major issue is the rapid decline of revaluation surplus. This buffer has almost been exhausted by the March 2026 quarter. Analysts warn that if yields rise further, banks may start losing core capital strength. In particular, Common Equity Tier-1 ratios could come under pressure. As a result, banks may need to rethink dividend payouts and adjust capital strategies.

Some of the largest banks are expected to take the biggest hit. United Bank Limited may face a post-tax impact of Rs117 billion on its book value. Meanwhile, Habib Bank Limited could see losses of Rs54 billion, and National Bank of Pakistan may record Rs45 billion in losses.

The pressure is largely linked to government securities exposure. Over time, banks have increased their share of floating-rate debt. This figure has now crossed 50%, compared to 36% in December 2021. Because of this shift, banks are more sensitive to interest rate changes and market spreads. This has increased volatility in their balance sheets.

Despite these losses, profitability may not fall sharply in the short term. Banks often benefit from higher rates as assets are repriced. However, the immediate impact is still negative. Capital buffers are under strain, and investor sentiment remains weak.

Looking ahead, the outlook is still uncertain. Support from the State Bank of Pakistan could help stabilize the sector. Meanwhile, some banks appear better positioned to handle the stress. MCB Bank, Bank Alfalah, Meezan Bank, and Faysal Bank have lower exposure to long-term fixed-income assets. Because of this, they are likely to recover faster as market conditions improve.