Pakistan has the largest gender gap in mobile money account ownership of any country surveyed in the GSMA’s latest global report, with women lagging behind men by a margin that dwarfs every other nation in the study.

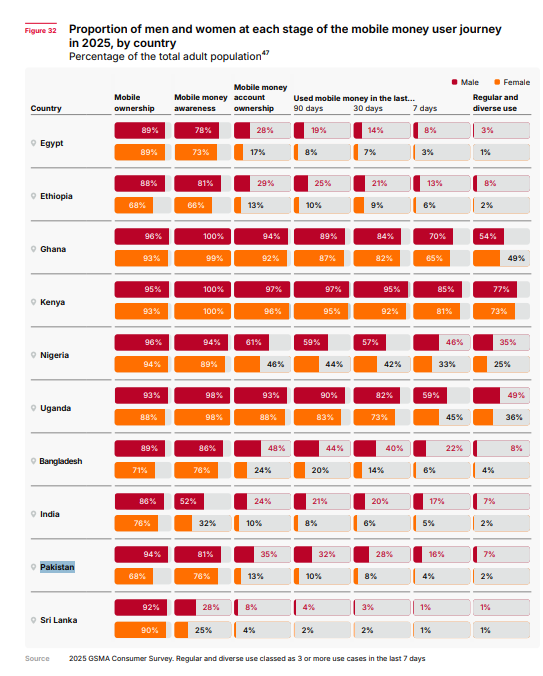

According to “The State of the Industry Report on Mobile Money 2026,” only 13% of Pakistani women own a mobile money account compared to 35% of men, producing a 63% gender gap. The report surveyed ten countries across Africa and Asia: Egypt, Ethiopia, Ghana, Kenya, Nigeria, Uganda, Bangladesh, India, Pakistan, and, for the first time, Sri Lanka. Pakistan finished last.

The barriers are layered and reinforcing. A strong preference for cash remains dominant, cited by 76% of women in Pakistan compared to 64% of men. Limited knowledge and digital skills compound the problem. But the most striking finding is social: 39% of Pakistani women reported family disapproval as a barrier to using mobile money, nearly three times the rate among men at 14%. In a country where household decisions about technology access are frequently made by male family members, this single statistic explains more about the gap than any infrastructure metric.

The divide starts before mobile money even enters the picture. Nearly one-third of Pakistani women still do not own a mobile phone, compared to just 6% of men. There has been some improvement. Women’s phone ownership rose by 10 percentage points since 2024. But a 10-point gain still leaves a gap so wide that millions of women remain excluded from the digital financial system entirely because they do not have the basic device needed to participate.

Geography amplifies everything. Pakistan’s rural gender gap in mobile money ownership reaches 74%, compared to 42% in urban areas. For women in rural Pakistan, the combination of no phone, no digital literacy, family resistance, and distance from formal financial services creates a near-total exclusion from the mobile money ecosystem that urban policy discussions often take for granted.

Usage patterns among those who do have accounts reflect the same disparities. Only 10% of women reported receiving customer payments in the past month, compared to 18% of men. Notable gender gaps in 30-day account activity persist in Pakistan alongside Egypt, Bangladesh, and India.

There are signs of progress in short-term engagement. The 7-day activity gender gap in Pakistan narrowed by 40 percentage points year-on-year, one of the largest improvements in the survey alongside Ethiopia and Nigeria. The 30-day activity gap, however, remained broadly unchanged, suggesting that while some women are using mobile money more frequently when they do engage, the overall base of active female users is not growing fast enough.

Pakistan’s position at the bottom of this ranking is not new, but the scale of the gap in the 2026 data makes it difficult to frame as a problem that is gradually resolving itself. The country has 190 million active SIM connections, a booming fintech sector, and a government that regularly invokes digital inclusion as a policy priority. Yet more than six out of ten women who could theoretically access mobile money do not, and for nearly four in ten of those women, the reason is not infrastructure or literacy but that their families will not allow it.

Closing a 63% gender gap requires more than app design improvements and awareness campaigns. It requires confronting the social dynamics that determine who in a household gets a phone, who is permitted to use financial services, and whose economic participation is treated as optional. Until those conversations happen at scale, Pakistan’s mobile money numbers will continue to describe two entirely different countries depending on whether the user is a man or a woman.

You can access the report here.