FinTech in Pakistan: Challenges, Opportunities and Recommendations

The report “Framework for rooting FinTechs in Pakistan” discusses the opportunities and gaps that exist in the FinTech eco-system of Pakistan and what can be done to promote it in the country.

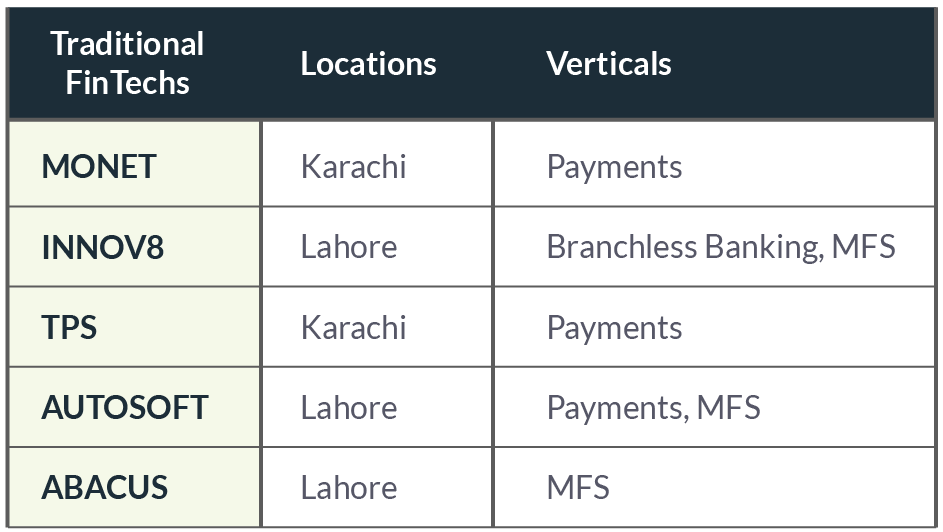

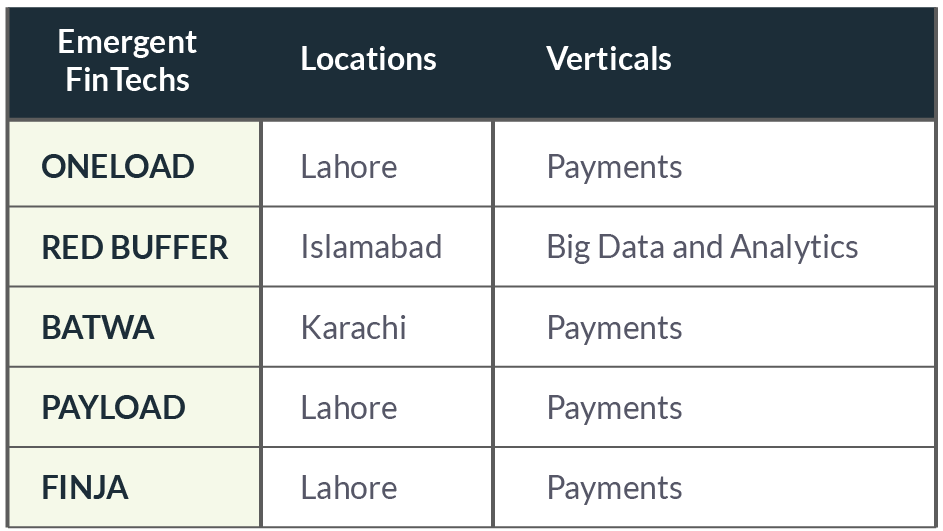

FinTech, short for Financial Technology, is the use of technology to provide financial services. What mobile apps are to smartphones, FinTechs are to financial service providers. FinTechs have been experiencing remarkable growth over the past few years globally. According to the report, FinTechs are categorized as:

“Traditional FinTechs collaborate with incumbent financial service providers as their technology providers through traditional pricing models.

Emergent FinTechs area new category of FinTechs that partner with a bank through new engagement models or simply displace financial institutions.”

Pakistan is mainly a cash-based economy. There is a lack of awareness about the importance of FinTech in Pakistan. 72% of the organizations do not know which FinTech are out there and looking to collaborate. For economies to transition to a cashless society and increase financial inclusion, new technologies, government programs and customer preferences are primary factors that facilitate this shift.

Gaps in Pakistan Market

Global FinTech investment is soaring every year while in Pakistan FinTechs face many challenges. Karandaaz Pakistan, a company which promotes financial inclusion by employing technology enabled solutions, and FinSurgent, a FinTech startup that focuses on harnessing emerging technologies in existing business models, have conducted a survey to identify the opportunities and gaps in FinTech ecosystem and future of digital financial services in Pakistan. Some of the gaps identified through the research are mentioned below:

Pakistan has a financial inclusion ratio of 15%, compared to an average of 33% for lower middle-income countries

The banking sector represents 80% of the financial services but serves only 15% of the population

1500 registered IT companies in Pakistan and technology services exported to other countries equate to $1.6 billion of total sales, but quality is lacking

Pakistan has low ICT access due to low per capita bandwidth and high entry level prices for fixed broadband plans

Pakistan ranks at 138 among 189 countries in the ease of doing business and has an Investment to GDP ratio of 15% compared to a 32% ratio of other emerging countries

12 players in Pakistan have branchless banking licenses of which none has interoperability among their wallets

Pakistan is one of the top 10 markets for remittances, but currently, these can only be collected from bank branches

Microfinance banks lack an extensive distribution system

Only 29% of women in Pakistan have smartphones, as compared to 77% of men

Challenges

FinTech industry in Pakistan faces many hurdles including a lack of larger organisation’s support, unfavorable regulatory environment etc. A list of challenges identified through a survey are:

Unreceptive attitudes of large players

Complicated and unfavorable regulations and

Deficient early stage funding

Lack of data security

Difficulty of licensing and access to license holders

Threat to intellectual property

Lack of mentoring

Lack of late stage funding for expansion

Difficulty in accessing customer base

Difficulty in attracting the right talent

Opportunities

With the world’s 5th largest young population and an increasing usage of internet and smartphones, Pakistani market shows the potential of adapting to the new financial technologies. The research points out favorable factors in Pakistan for FinTech growth:

With a mobile penetration of 69%, Pakistan is quickly becoming an economy reliant on mobile phone technology

Smartphone adoption is expected to rise from 16.6% in 2016 to 51% by 2020

Pakistan only had 7.33 ATMs per 100,000 people in 2014. However, it can leap to the next generation of digital payments infrastructure and bypass the physical payments infrastructure

With 132 million biometrically verified SIMs, issuing wallets is possible through the click of a button

Insurance companies want to reach customers and make sales via online channels as well as collect premium payments digitally

Pakistan’s e-tail is expected to grow to EUR 746 million by 2019 EUR 1.9 billion by 2024 – a 2.3% penetration

Pakistan is considered to be almost 73% urban or urbanizing; these areas are connected physically and electronically and promise a high rate of FinTech adoption

Recommendations

FinTech industry has a huge potential to grow in Pakistan. The researchers recommend following:

Provide necessary FinTech coaching

Building FinTech awareness programs and collaboration platforms

Eliminating the regulatory ambiguity

Need for a FinTech consortium

Need for neutral FinTech incubators

Digital payment infrastructure and not cash distribution infrastructure will lead the transition to the new age of financial products and services

Branchless banking interoperability will provide further impetus to move from cash to digital

M-wallets trump plastics (credit and debit cards) as the digital payment method which can truly enhance customer experience and give a further boost to growing m-commerce

Pakistan, 6th largest population in the world, provides an excellent opportunity for FinTechs to grow and operate and contribute to the country’s economic and GDP growth. It is the need of the hour to not only invest and support the local upcoming FinTechs in the country but to create an environment conducive to the growth of FinTechs in Pakistan.

{kind=link}

{kind=link}